New Kenya NSSF Rates 2026 Mean Thinner Payslips

The new Kenya NSSF rates for 2026 are set to kick in next month, and many workers are already bracing for smaller take-home pay. Starting in February, the National Social Security Fund will bump up the earnings limits for contributions. That means higher deductions for a lot of salaried people, especially those earning decent money. It’s all part of the ongoing rollout of the 2013 NSSF Act, now in its fourth year.

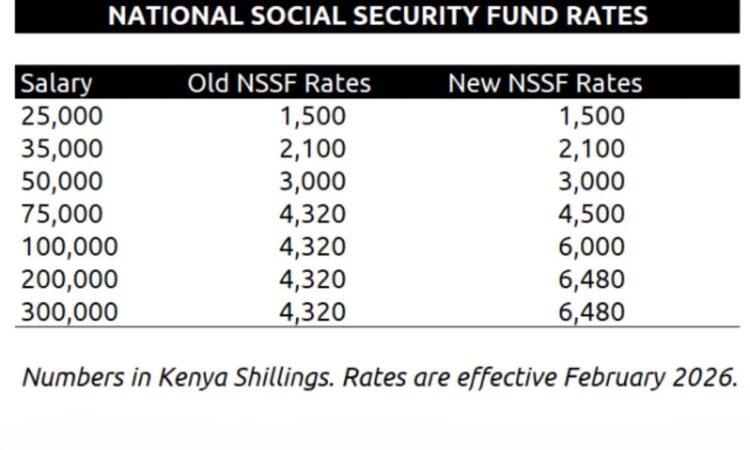

The changes aren’t about raising the percentage – it stays at six percent from the employee and another six from the employer. What shift is the salary range they apply for? Right now, the lower limit sits around KSh 8,000, but come February, it jumps to KSh 9,000 for Tier I. That’s the basic part: everyone pays on their first pay cheque. For Tier II, the upper cap goes from KSh 72,000 to a whopping KSh 108,000.

What does that look like in real numbers? If you earn more than KSh 108,000 a month, your NSSF deduction will top out at KSh 6,480 – up from the current KSh 4,320. Employers match that amount. For someone pulling in KSh 100,000 or so, the hit will be noticeable right away. Lower earners, say under KSh 50,000, might not feel much difference since their full pay already fell inside the old limits.

President William Ruto has backed these hikes before, calling the old flat KSh 200 contributions a joke. He argues better savings now mean stronger pensions later, especially as people live longer after retirement. The fund itself has grown big time – assets hitting over KSh 500 billion, with yearly inflows pushing toward KSh 100 billion soon.

But not everyone’s cheering. In offices and factories, workers grumble about yet another bite out of their salary. With the cost of living still high – food prices up, rent biting, school fees looming – this feels like bad timing. Unions have complained in the past, saying, ‘Force more savings when people struggle to eat today.’ Some point to past scandals at NSSF and wonder if the money is truly safe.

Small business owners aren’t thrilled either. They have to match every shilling deducted from staff, adding to payroll costs. In a tough economy, that might mean slower hiring or holding back on raises. One employer in Nairobi shared how he’s already crunching numbers to see the impact come February payslips.

The setup is tiered to make it fairer. Tier I covers basic wages up to KSh 9,000 – that’s KSh 540 from each side. Then Tier II kicks in for earnings above that, up to the new KSh 108,000 cap. Anyone below the lower limit still pays on what they earn, but most formal jobs start higher anyway.

NSSF bosses say the goal is simple: build a bigger nest egg for retirement. Kenya’s population is young now, but that won’t last forever. More money in the fund means better benefits down the line, like monthly pensions that actually cover basics. They’ve pointed to the jump in collections as proof the system works.

Still, for everyday Kenyans queuing at ATMs or shopping in markets, it’s hard to see past the immediate pinch. Social media is full of calculations – how much less in the pocket and what it means for weekend plans or kids’ needs.

The government insists this phase had to happen. Delaying again would only push problems further. They’ve highlighted how contributions are tax-deductible, softening the blow a bit on net pay. And for the vast majority earning under KSh 100,000, the change isn’t drastic.

As February approaches, payroll teams are busy updating systems. Employers got reminders to adjust before the deadline. Late payments mean penalties, so no one wants to slip up.

In the bigger picture, these new Kenya NSSF rates for 2026 tie into efforts to secure old age for workers. Other levies like housing and health insurance already trim payslips. Together, they aim for a safer future, but right now, many just feel the squeeze.

Workers in estates chat about it over tea. “How do they expect us to save more when we barely make ends meet?” one asked. Others nod, hoping the long-term payoff proves worth it.

For now, payslips tell the story – a few more lines of deductions, a little less to spend. Come March, when the first adjusted salaries hit bank accounts, the real talk will start. Whether it builds resentment or quiet acceptance, only time will tell. One thing stands out: retirement planning isn’t optional anymore. The new rates drive that home, whether Kenyans like it or not.

Related Posts

Lumumba Vea Signs Rexona Deal at 2026 World Cup

Congolese superfan Lumumba Vea signs Rexona deals with the 2026 World Cup in Mexico after his motionless tribute pose captured global attention. The passionate supporter…

Doky Dorcas Sets New Guinness Record for Fastest Chapatis

Doky Dorcas claimed the title for the fastest chapatis when she whipped up three fresh ones in record time at Ongata Rongai on December 15,…

Ruto Fires Back at Gideon Moi Accusing Him of SG Media Headlines…

President William Ruto hit out sharply at Gideon Moi and Standard Media over what he calls daily extortion through headlines. The strong social media post…

Banking for Business Growth – Don’t Miss This Masterclass By Co-op Bank

Starting and growing a business comes with many opportunities, but it also requires the right financial support to succeed.Join us this Friday as we explore…